AMD today: the trend is real, but the stock is already very hot

As of the April 17, 2026 US close, AMD finished at $278.39, only about 0.6% below its 52-week high. If you are trying to decide what to do with the stock here, the useful questions are not abstract. You need to know whether the trend is still healthy, whether the setup is already too stretched, whether institutions are still aligned, and what the May 5 earnings report could change.

Key takeaways

- • As of the April 17, 2026 US close, AMD finished at $278.39, up 13.61% in one week and 39.57% in one month, only about 0.59% below its 52-week high.

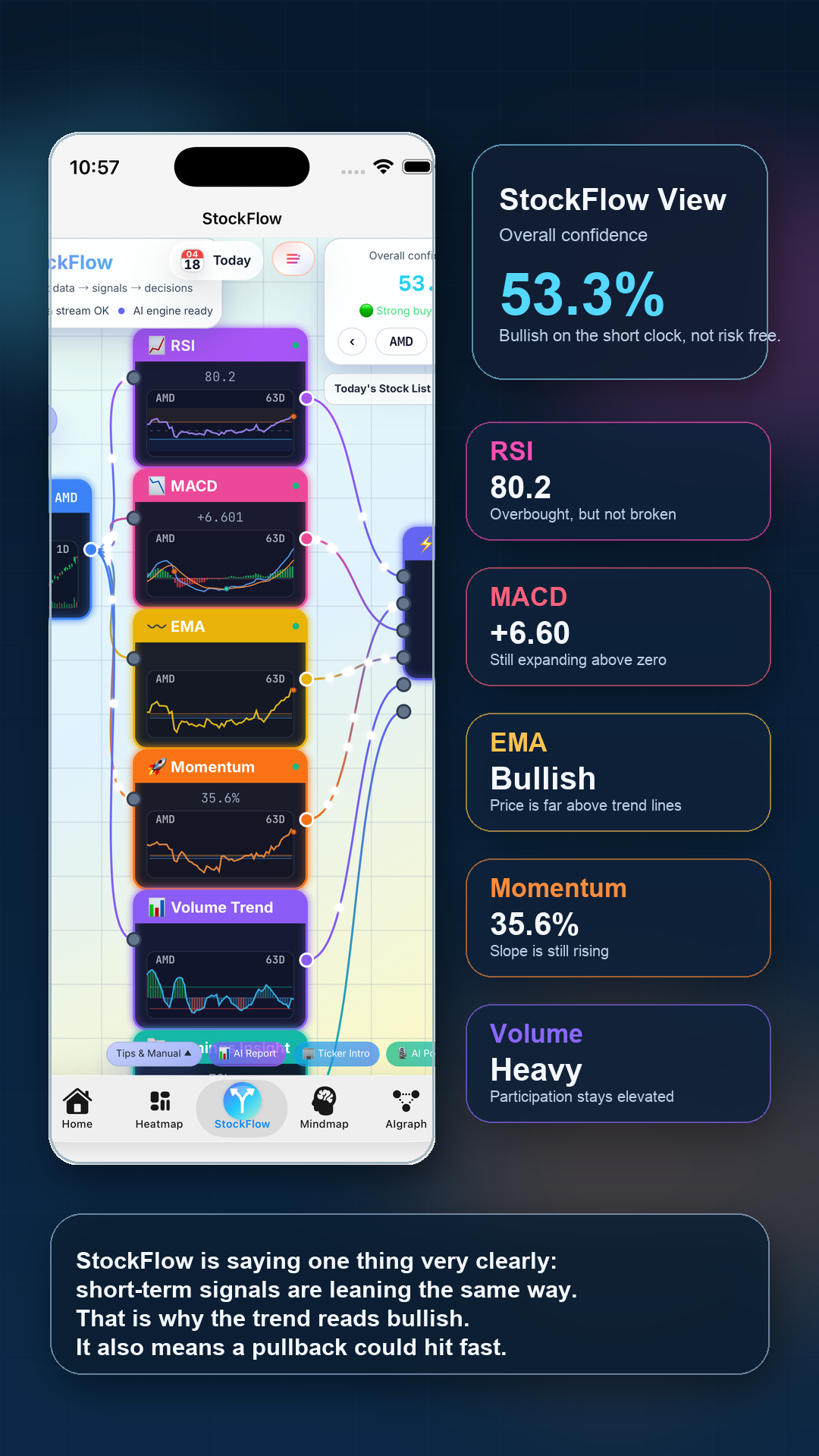

- • StockFlow overall confidence reads 53.3%, and price remains well above the 20-day EMA, 50-day EMA, and 200-day average.

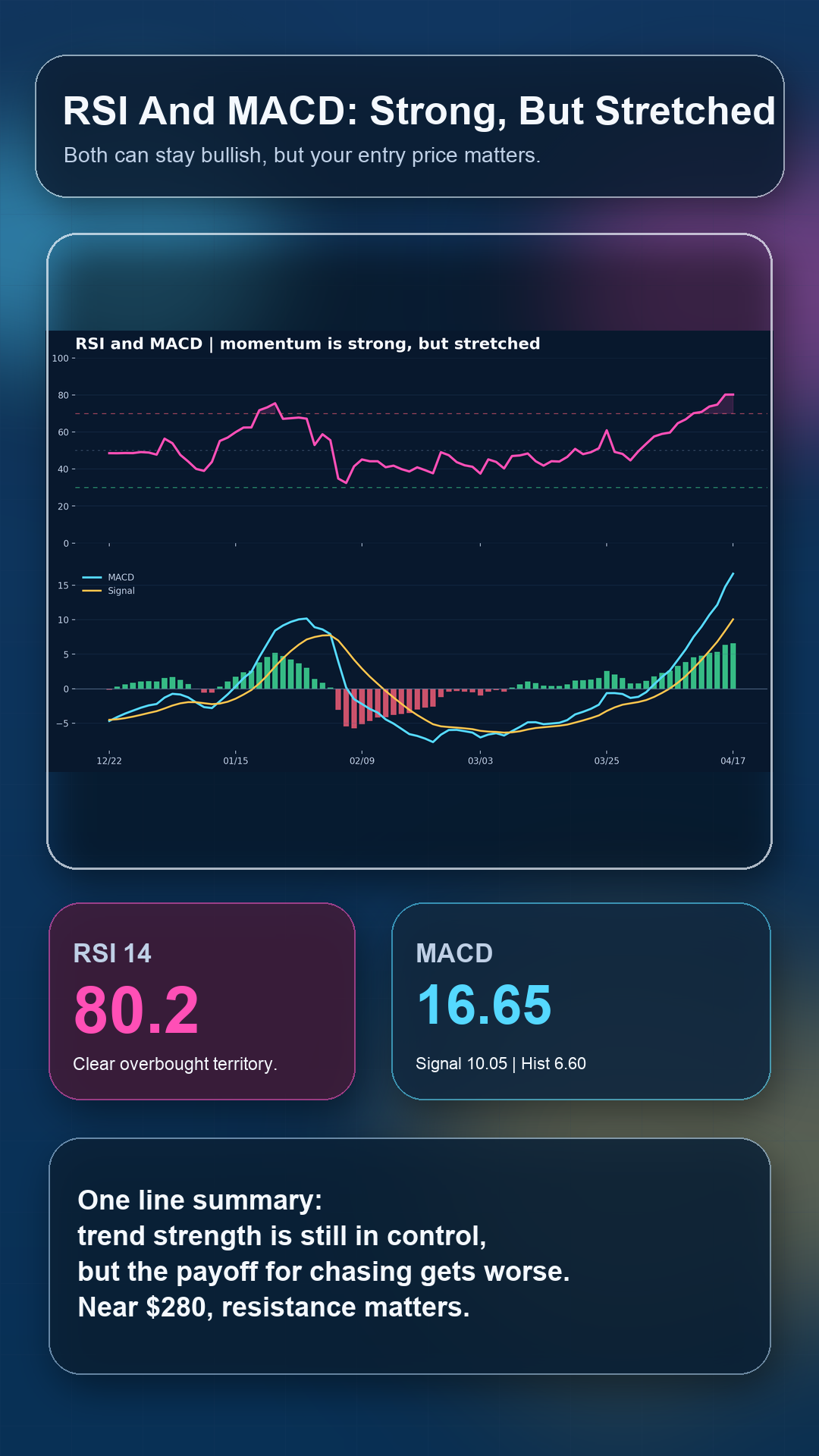

- • RSI14 at 80.2 and a widening MACD say the trend is still strong, but also crowded and stretched.

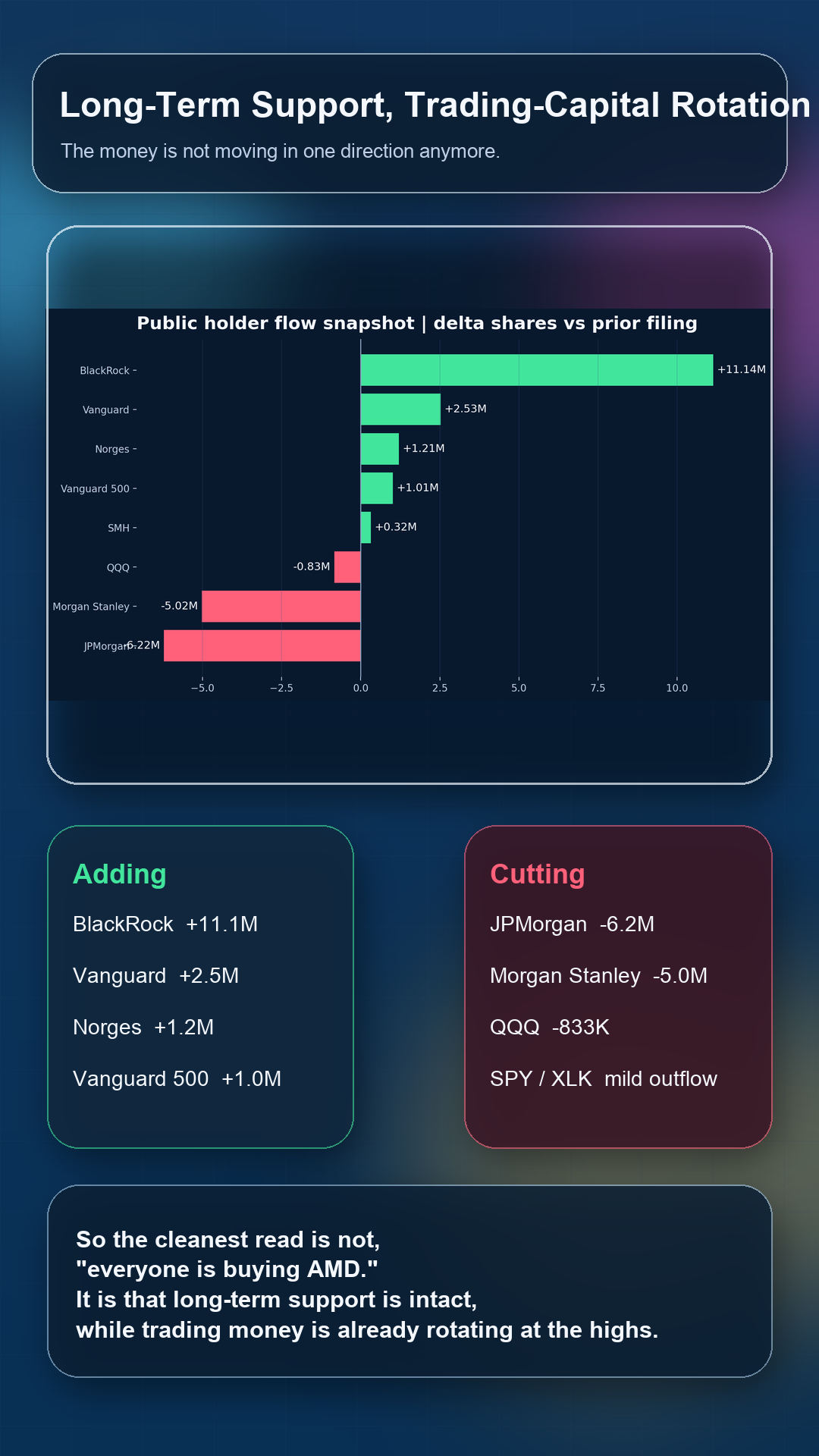

- • Institutional ownership is about 72.2%. BlackRock and Vanguard are still adding, while JPMorgan and Morgan Stanley have already been reducing.

- • The next real decision point is AMD's May 5, 2026 earnings report, not the current emotional high in price.

Where AMD sits right now

At the April 17, 2026 US close, AMD was no longer behaving like a normal bounce candidate. The stock finished at $278.39, up 13.61% in one week and 39.57% in one month, while sitting only about 0.59% below its 52-week high. That is how a market treats one of the strongest trend names in the group.

But a strong trend is not the same thing as an easy risk-reward setup. From the user side, the more useful question is whether this is still a position you can ride, or whether it is already so hot that the next move matters less than the next pullback.

Sources: AMD quote page

Why this is not a normal bounce anymore

The structure is straightforward. AMD is up 13.61% in one week and 39.57% in one month, while closing well above the 20-day EMA at 235.21, the 50-day EMA at 221.75, and the 200-day average at 202.45. That tells you the short-term pace, medium-term trend, and bigger-picture direction are all still aligned.

The short-term StockFlow stack reads 53.3% overall confidence. That is not a euphoric maxed-out reading, but RSI, MACD, EMA positioning, momentum, and volume are all leaning to the same side. In practice, the setup is still bullish, just no longer cheap.

Sources: AMD quote page

Why I still would not chase this level blindly

The main risk is not that the trend has already broken. The problem is that the trend is now very hot. RSI14 is at 80.2, clearly above the usual overbought line around 70, while MACD continues to widen above zero. That combination says momentum is still alive, but it also says a lot of optimism is already priced in.

Put differently, AMD now looks like a high-beta uptrend, not an early low-risk setup with wide tolerance. If you already own it, the key question is whether pullbacks stay orderly. If you do not own it, waiting for a better digestion phase or for earnings confirmation usually offers cleaner asymmetry than buying into peak enthusiasm.

Sources: AMD quote page

Institutions are still supportive, but the faster money is already split

Institutional ownership is about 72.2%, which tells you AMD is not trading like a loose retail-only momentum name. On the latest public holdings boundary, Vanguard held about 158.5 million shares, BlackRock about 147.5 million, and State Street about 74.9 million. The long-duration ownership base is still very heavy.

But the flow direction is not one-way. BlackRock added about 11.1 million shares, Vanguard added about 2.5 million, and Norges Bank also added. At the same time, JPMorgan cut about 6.2 million shares and Morgan Stanley cut about 5.0 million. That is a useful distinction: the long allocators are still supportive, but the more tactical capital is already de-risking on strength.

Sources: AMD holders page, AMD institutional ownership overview

The next real decision point is May 5 earnings

If you only look at price, AMD does seem close to discounting a lot of good news already. But the fundamental backdrop is not fake. In its February 3, 2026 Q4 2025 release, AMD reported record quarterly revenue of $10.27 billion, with $5.38 billion from Data Center and $3.94 billion from Client and Gaming. That is why the stock has been rewarded: the business base really did get bigger.

The more important issue is quality of earnings. AMD also said Q4 benefited from roughly $360 million of previously reserved MI308 inventory and related charge reversals, plus about $390 million of MI308 revenue to China. Excluding those effects, Q4 non-GAAP gross margin would have been about 55%, not the headline 57%. That is why the May 5, 2026 earnings report matters so much: the market needs to see whether AI and Data Center growth can keep compounding at a cleaner margin level. The enlarged buyback authorization still supports the capital-allocation backdrop as well.

| Item | Latest disclosed number | Why it matters |

|---|---|---|

| Q4 2025 revenue | $10.27B | AMD is now operating from a meaningfully larger earnings base. |

| Q4 2025 Data Center revenue | $5.38B | Data Center is now the core growth engine. |

| Q4 2025 Client & Gaming revenue | $3.94B | The story is broader than AI enthusiasm alone. |

| Q4 2025 non-GAAP gross margin | 57% | The headline is strong, but it should not be treated as a permanent clean run rate. |

| Q4 normalized non-GAAP gross margin | about 55% | That is closer to the cleaner baseline investors should underwrite. |

| Q1 2026 revenue guidance | about $9.8B ± $0.3B | The next major market test will be judged against this baseline. |

| Q1 2026 non-GAAP gross margin guidance | about 55% | Management is already guiding back toward a more normal margin level. |

Sources: AMD Q4 2025 and full-year 2025 results, AMD Q1 2026 earnings date, AMD share repurchase authorization

What to watch next

- • Whether AMD can digest this run without breaking the 20-day EMA or otherwise damaging the short-term structure.

- • Whether May 5 earnings can sustain Data Center and Instinct momentum while keeping non-GAAP gross margin around the cleaner 55% zone.

- • Whether institutional flow divergence widens further, or tightens again into earnings.